Selling your home is freedom — a new life, a fresh start, and maybe even some money in your pocket. But before you bid adieu to your home, another house party can look forward to claiming some of your joy: the Internal Revenue Service. If you’ve made a sale of a home, you might need to report it to the IRS, depending on how much profit you made, how long you lived in the house, and whether or not you were issued a special form known as a 1099-S. Let us go through step by step on all that you will want to keep in mind to not be caught off guard later.

🏡 Step 1: Do You Need to Report It?

You are obligated to report the sale of your home if one of the following is true:

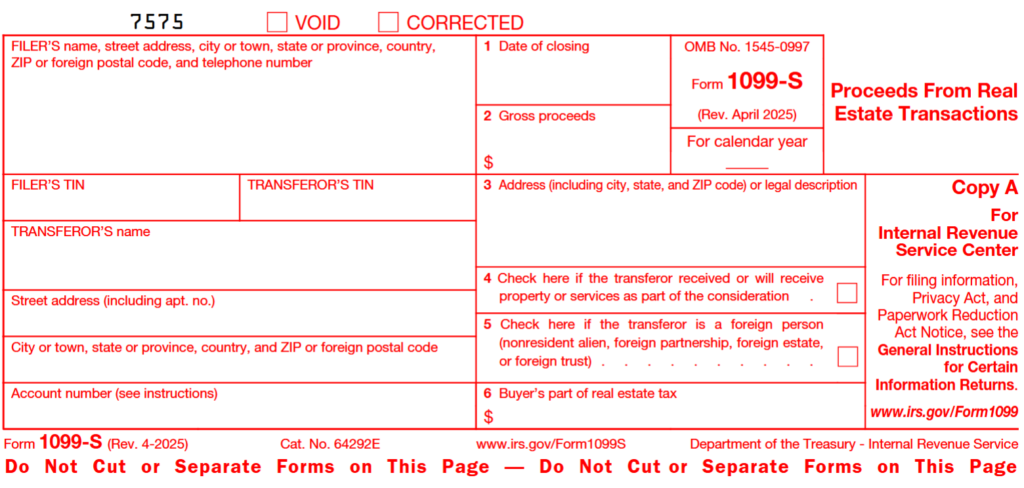

- You have been issued a Form 1099-S by your title company, attorney, or real estate agent.

- You made a gain that is not fully excluded under the IRS home sale exclusion rules.

- You rented out or used your home as a business.

If you did not get a 1099-S and your entire profit qualifies for exclusion, you usually do not have to report it.

💰 Step 2: What is “Gain” and “Exclusion”?

Your gain is simply your profit from selling the home.

It is what you sold it for minus its cost basis.

Formula:

Selling Price – Selling Costs – Adjusted Basis = Gain

Your starting point is the amount you initially paid, plus major home upgrades like new kitchens, roofs, or additions, less depreciation if used for business or leased out..

The IRS allows you to exclude up to $250,000 of gain if you are single, or $500,000 if you are married filing jointly, as long as:

- You lived in the house for more than 2 years, and

- You consider it as your primary residence for at least 2 years during the 5 years preceding the sale.

If your profit is below these limits, your gain is fully excluded; therefore, you owe no tax.

⚖️ Step 3: When You Must Report?

If your gain is more than the exclusion or you received a Form 1099-S, you must report the sale.

Here is how:

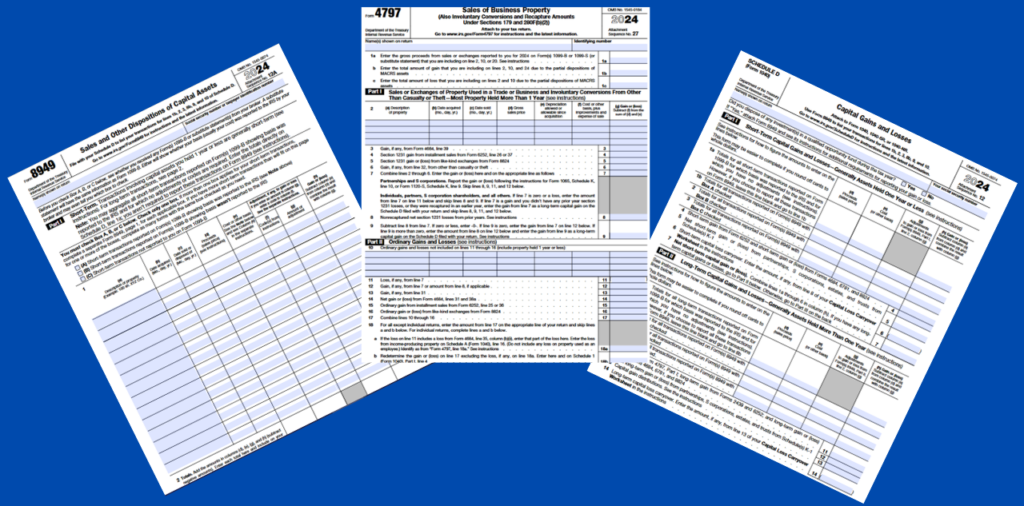

- Form 8949 – Report details of the sale (address, purchase and sale dates, selling price, and cost basis).

- Schedule D – Summarize total capital gains and losses.

- Write “Section 121 exclusion” on the form to show how much of the gain you excluded.

If you received Form 1099-S, you must report the sale even if your gain is completely excluded.

This tells the IRS that you accounted for the transaction properly.

🧠 Step 4: Example of Reporting

Example 1 –Gain Totally Excluded:

You bought your home for $200,000, sold it for $450,000, and paid $25,000 in selling costs.

Your gain is $225,000.

Because you are single, and the exclusion limit is $250,000, you can exclude the entire gain.

If you did not receive a 1099-S, you do not have to report the sale.

Example 2 – Partially Excluded:

You bought your home for $300,000, sold it for $900,000, and paid $50,000 in selling costs.

Your gain is $550,000.

If you are married filing jointly, you can exclude $500,000, but the remaining $50,000 is taxable and must be reported — even if you did not receive a 1099-S.

🏠 Step 5: Keep Every Record

The IRS might ask for documents:

- Purchase and sale closing statements

- Receipts for major home improvements

- Form 1099-S (if applicable)

- Mortgage or utility statements as proof of residence

These documents are your evidence of any discrepancies later.

💡 Step 6: When You Do Not Report

You do not have to report your sale of your home if:

- You did not receive a 1099-S, and

- Your whole gain is Section 121 qualified.

Then the IRS does not require you to report the sale on your tax return.

🚫 Step 7: What If You Sold at a Loss?

Simply, the IRS does not care for your loss. You do not report it at all. The IRS can not tax on losses.

🏢 Special Case: Condominiums

The same applies if your home was a condo. Condos are qualified for the same sale of home exclusion if you had it as your primary residence.

However, if you rented it out before sale, you will owe income taxes on recaptured depreciation, and this is not excluded under Section 121.

To summarize. If you get Form 1099-S or have taxable gain, you must report it. If your gain is fully excluded and no form was issued, you do not report it.

| Situation | Must You Report? | IRS Forms Needed | Tax Due? |

|---|---|---|---|

| No 1099-S and full exclusion | No | None | No |

| Received 1099-S (even if excluded) | Yes | Form 8949, Schedule D | Possibly |

| Gain exceeds exclusion | Yes | Form 8949, Schedule D | Yes |

| Rented or used for business | Yes | Form 4797, Schedule D | Partial |

| Sold at a loss | No | None | No |